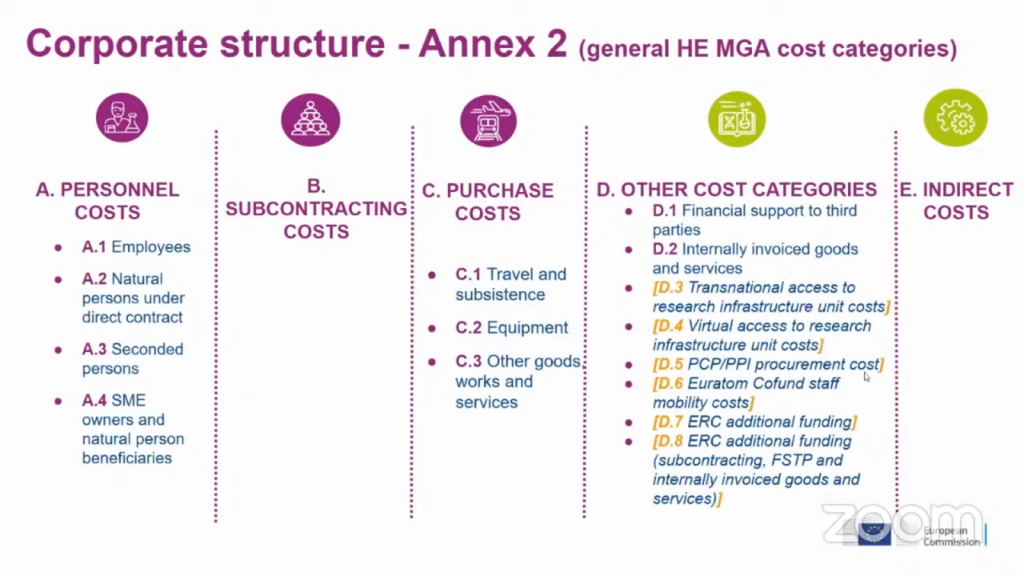

Horizon Europe defines five main categories of eligible costs, as outlined in Article 6.2 of the General Model Grant Agreement (GMGA). Below is an overview of each category, including specific eligibility conditions.

A. Personnel Costs

Eligible personnel costs include:

- A.1 Employees or Equivalent

Costs for employees working under an employment contract (or equivalent appointing act), assigned to the action, and meeting general eligibility conditions. - A.2 & A.3 Non-employees and Seconded Staff

Costs for:- Natural persons working under a direct contract other than an employment contract, and

- Persons seconded by a third party against payment.

These costs are eligible if the persons are assigned to the action and meet general conditions.

- A.4 SME Owners and Natural Person Beneficiaries

SME owners or individual beneficiaries not receiving a salary may declare their work as personnel costs, if calculated as unit costs in accordance with Annex 2a, and all general eligibility conditions are fulfilled.

B. Subcontracting Costs

Subcontracting costs are eligible if:

- They are necessary for the action,

- Calculated based on actual costs incurred (including related non-deductible VAT), and

- Awarded using the beneficiary’s standard procurement procedures ensuring best value for money and avoiding conflicts of interest.

See Article 12 of the GMGA for procurement rules.

C. Purchase Costs

These costs cover purchases made specifically for the project. They are eligible if:

- Incurred in accordance with usual purchasing practices,

- Ensure best value for money (or lowest price), and

- Avoid conflicts of interest.

C.1 Travel and Subsistence

Costs for travel, accommodation, and subsistence are eligible if based on actual costs and in line with the beneficiary’s standard travel policy.

C.2 Equipment

Costs for equipment, infrastructure, or other assets must be declared as depreciation costs, calculated based on:

- Actual cost,

- Duration and rate of use in the project,

- International accounting standards and usual practices.

Renting or leasing is also eligible if:

- Costs do not exceed depreciation of similar assets, and

- No financing fees are included.

C.3 Other Goods, Works, and Services

Includes consumables, promotion, dissemination, translation, result protection, publications, and financial guarantees. Costs must be based on actual expenditure.

Public bodies (contracting authorities) must also comply with applicable national public procurement laws.

D. Other Direct Costs

These are additional categories specifically allowed under certain conditions:

- D.1 Financial Support to Third Parties

Eligible only if foreseen in the call conditions and provided as grants, prizes, etc., following rules in Annex 1. - D.2 Internally Invoiced Goods and Services

Eligible as unit costs when aligned with usual cost accounting practices and declared eligible in the call.

Other specific cost categories include:

- D.3 Transnational Access to Research Infrastructure

- D.4 Virtual Access to Research Infrastructure

- D.5 PCP/PPI Procurement Costs

- D.6 Euratom Cofund Staff Mobility Costs

- D.7 ERC Additional Funding

- D.8 ERC Additional Funding (Subcontracting, FSTP, Internally Invoiced Services)

Check the specific call conditions to confirm eligibility for these categories.

E. Indirect Costs

Indirect costs are reimbursed using a flat-rate of 25% of the total eligible direct costs (Categories A–D), excluding:

- Volunteers’ costs

- Subcontracting costs

- Financial support to third parties

- Any other excluded categories listed in the Grant Agreement

📘 Reference

- GMGA Article 6.2 – Specific eligibility conditions for each budget category

(Costs eligible in Horizon Europe)